Cash flow. It’s the lifeblood of every business and for retailers, it’s no different. In a competitive industry where consumer demands are becoming increasingly hard to satisfy, cash flow management for retailers can be a struggle.

In fact, to put it in perspective: 23% of small businesses in the US report lack of cash flow as their main challenge. Factors that contribute to a lack of cash flow can vary, from slow-moving inventory to rising interest rates and supplier costs. Some of these factors may be out of your control, but there are still ways you can not only improve, but increase cash flow.

That’s why in this article, we’re going to provide cash flow tips and guidance for retailers.

Here’s what you’re going to learn:

- What cash flow management is

- Cash flow vs. profit

- Why managing cash flow is important

- How to forecast and manage cash flow

- How to improve cash flow [in 7 ways]

Let’s get started!

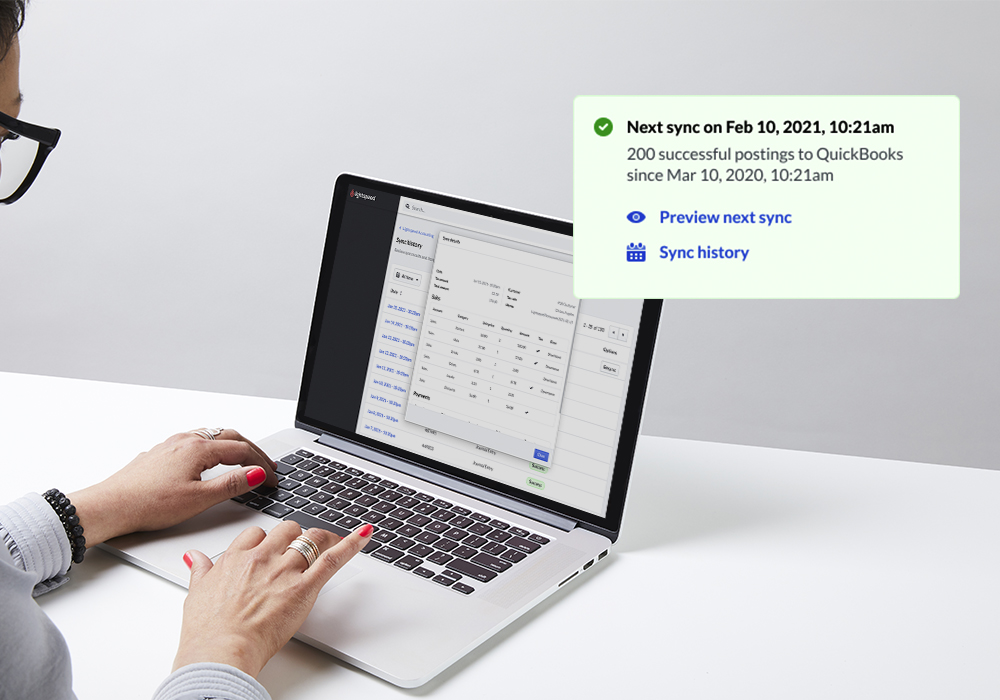

Get complete visibility of your store's finances

With Lightspeed, you can sync your point of sale and accounting software and have completely accurate, automated bookkeeping.

What is cash flow management?

Put simply, cash flow is the amount of money that is coming in and out of your retail business.

When your customers buy something from your business, you get paid. A lot of hard work goes into making those sales happen—with cash flowing out in the other direction on expenses such as wages, supplies, materials, distribution, marketing and much much more.

Your cash flow is positive when your business has more sales and income coming in then it does in a wide range of business expenses.

Cash flow management is about monitoring, studying and tweaking your cash receipts and expenses. Let’s look in a little more detail at some significant aspects of cash flow management.

Positive vs. negative cash flow

Positive cash flow: Your cash flow is positive when your business has more sales and income coming in than it does in a wide range of business expenses. This means that your business can cover expenses and has excess funds to reinvest in the business, set aside and more.

Negative cash flow: Your cash flow is negative when your business is spending more than it’s earning. If your cash flow is consistently negative, you may face financial difficulties or business failure in the future.

Important components of cash flow management

Monitoring cash flow

Accounting software, manual ledgers or an expert advisor can all go far when it comes to regularly tracking all your cash inflows and outflows.

Using this information, you can create cash flow statements that provide a clear and accurate picture of your retail business’s financial health. For optimal organization, categorize cash flow statements over specific periods: such as monthly, quarterly and annually.

In terms of your method, retail accounting software can make the process more efficient for you. Lightspeed Accounting, for instance, helps you save time and reduce errors so your books are always accurate and up-to-date.

Studying cash flow patterns

It’s not enough to just track cash flow over current time periods. Analyzing historical cash flow data can help you identify trends and patterns, allowing you to plan for the future. For instance, seasonal variations may lead to higher sales certain times of the year, while other months may have lower sales and higher expenses.

These insights can help you forecast future cash flows, allowing you to anticipate periods of surplus or shortfall. Plus, inventory management becomes more streamlined when you factor in historical cash flow patterns.

The difference between cash flow and profitability

But wait. Here’s a quick pointer before we go on. Cash flow and profit aren’t the same.

Profit is more of an accounting principle.

It’s what’s left after taking away all expenses your business incurred while generating its revenue.

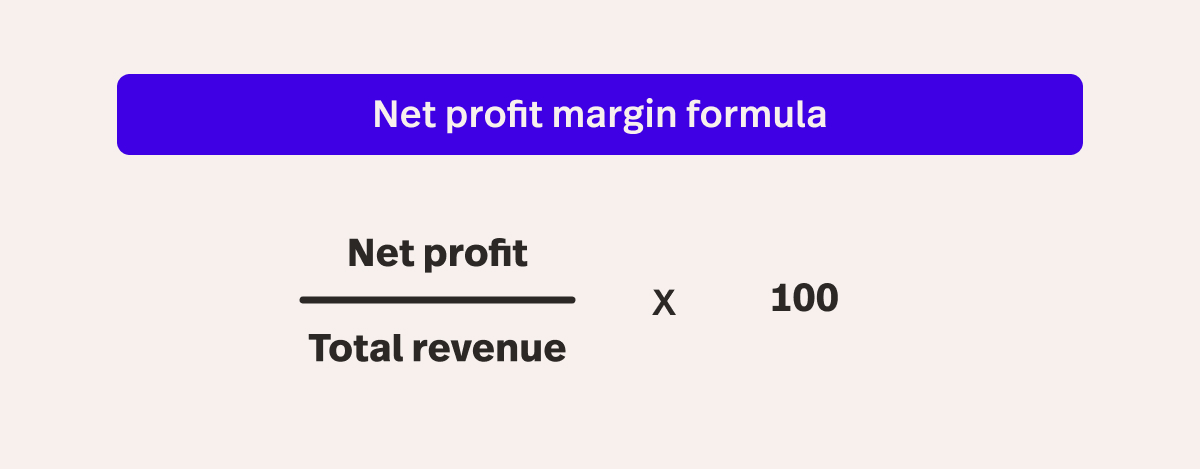

How to calculate net profit

Here comes the math. Just a small bit, though.

Net profit is typically given as a percentage, not a dollar figure. To get the net profit percentage, divide your net profit by your total revenue and multiply the result by 100. Here’s the formula:

Why cash flow management is important

Let’s leave profit aside again and talk more about cash flow.

It’s critical for all businesses.

Time and time again, it’s the leading reason businesses fail. Businesses globally experiencecash flow problems, according to recent QuickBooks research. Just under a third said they couldn’t pay themselves, vendors or lenders, because of poor cash flow.

Why retail cash flow management matters

What about retail, specifically?

“The key to managing cash flow for retailers is really related to two things — how quickly they turn their stock and how much gross profit they are making on each sale,” explains Catherine Erdly, founder of Future Retail Consulting.

“Monitoring and maintaining a healthy gross profit margin on every sale will ultimately allow enough cash to flow through the business,” says Erdly. “One of the main culprits when it comes to poor cash flow management is when the amount of profit on every sale is not enough to cover the other costs in a business.

“Another difficulty with cash flow stems from poor stock management. Buying too much upfront, failing to clear slow-selling stock and overcommitting to stock, in general, will all create significant problems with cash flow.”

If you want to dive deeper into how to calculate and improve your store’s gross profit margins, read our article How Retailers can Increase Profit Margins: 20 Proven Ways to Improve Profitability.

Five ways sound cash flow can help retailers

Here’s how well-managed cash flow can help your retail business overcome those kinds of problems.

1. Protect against sales shortfalls

Retail cash management is a particularly challenging responsibility. It costs a lot to source retail inventory, pay good staff and keep operations running in brick and mortar and online stores.

Just think of a large clothing retailer who is trying to plan inventory for summer in winter.

What if that business is operating in a region where the weather is unpredictable? The business may have stocked its stores with extra shorts and swimwear, only to find people aren’t buying these clothes because it’s been cloudy and rainy for weeks.

That’s the kind of unexpected event that could cause the retailer to go out of business if it doesn’t have a solid cash flow projection.

2. Reduce owner and staff stress

Not knowing if you can pay yourself, your staff or your suppliers is an awful situation for any business owner to be in. Getting a handle on your current and projected cash flow—so you know who can be paid and when—can help keep everyone’s stress levels in check.

3. Know where and when to grow

Without a solid grasp on cash flow, it’s impossible for a business to understand how and when it can grow. Growth for growth’s sake is often touted as a pure positive by media headlines. But it’s important to look at it with a clear head.

Growing a retail business can come with a host of expenses around inventory, distribution, product development and marketing. Knowing exactly what cash you have on hand can help you make wise decisions about growing—and shrinking—your business, as needed.

4. Improve supplier relationships

Maintaining a positive cash flow ensures that suppliers are paid on time. That can result in better terms, discounts and priority service. Strong supplier relationships can also provide leverage during negotiations for improved prices or extended payment terms.

Plus, being able to pay suppliers in advance of due dates can positively impact your relationships and even lead to better deals.

5. Open the door for investment opportunities

Well-managed cash flow provides you with the flexibility to take advantage of investment opportunities as they arise. This could include buying inventory at a discount, purchasing new technology, or expanding into new markets, all of which can drive growth and profitability.

Not only that, but you can also invest in improved customer service and better inventory tracking. That way, customer satisfaction increases and you’ll ensure that popular products are always in stock, to keep them coming back.

Ultimately, you can make better decisions for your business to boost sales.

How to forecast and manage cash flow

So, the benefits are clear.

Now let’s delve a little deeper into cash flow management.

What is a cash flow statement?

Let’s start with the cash flow statement.

A cash flow statement is a financial statement that lists all the inflows and outflows of cash in a business, according to Investopedia. It’s considered as one of the three main financial statements for any business, along with the income sheet and balance statement.

How to create a cash flow statement

So how do you go about creating one?

Firstly, don’t worry about starting from scratch. There are plenty of free templates online, like this cash flow statement template from QuickBooks, which includes some helpful notes on adding your data.

Working with your template, here’s what you’ll need to do.

1. Forecast expenses

Collect every single business expense you have records of, such as:

- Payment processing fees

- Merchant account fees

- Postage and delivery fees

- Telephone and internet

- Insurance premiums

- Website development

- Legal and accounting

- Salaries

2. Forecast revenue

And also collect every piece of data you have on your retail business’s revenue, such as:

- Cash sales

- Payments from customer credit accounts

- Loans or other finance

- Any interest income

- Any tax refunds

3. Input your data

Once you’ve gathered all this data, put it into your cash flow template.

Your cash flow statement should include sections for the following:

- Your beginning cash on hand

- Individual and total cash payments

- Individual and total cash receipts

- Your operating expenses

- Other expense payments

- Your total cash payments

- Your net cash change

- And your cash position

If you’re unsure where to place what, get support from a bookkeeper or accountant.

How to improve cash flow: seven strategies

Now that you have a sense of how to record your retail business’s cash flow, let’s look at some steps you can take to increase your cash flow—and with it your control and confidence in your business’s cash position.

1. Carefully manage your stock

Clever inventory management is a key part of cash flow management.

The simplest way to look at this would be to make sure you sell only products that people want to buy (tip: use your point of sale system’s sales reports to pinpoint products with high turnover).

But that’s enough. There may be people demanding your store stock a certain type of product. That’s well and good, but there need to be enough people regularly and predictably buying particular products.

This is why retail business-owners and the finance teams need to be careful about what they stock and how much they stock. Otherwise, your business will be left with excess stock that it can only shift with extreme discounting.

The right retail inventory management software can help you tremendously. Lightspeed Inventory Management allows you to directly connect with suppliers, avoid out-of-stocks, speed up ordering and track inventory across all your channels from one screen.

Strong inventory management in action

Lightspeed retailer and franchise Apricot Lane Boutique exemplifies the importance of good inventory management.

“Understanding the performance of your inventory is critical. We teach our owners how to really dive into the performance of their product through a disciplined, open to buy process,” company CEO Chris Lanning says.

“The reporting that Lightspeed provides us, they’re able to see by category what’s working, what’s not working. This helps them unlock the potential that exists within their inventory.”

Knowing exactly what’s working for your business when it comes to product performance, sales and stock counts can transform your cash flow.

What POS system is the best fit for you?

Learn what questions to ask as you shop different options with our free POS Buyer's Guide. Discover how to plan your store’s growth and choose a POS system that can support your business now and in the future.

2. Cut some fixed and variable expenses

Rent, phone, internet and salaries are some of the fixed expenses across the financial year.

In retail especially, you’re going to have plenty of variable expenses too—such as shipping fees, material and stock purchases. To look at reining in these expenses, ask yourself:

- Are you getting the best possible deal as a commercial tenant?

- Can you cut fixed telecommunications costs by switching providers?

- Is the business staffed at the right level? How can you optimize staffing based on peak sales periods?

3. Review insurance policies

You need insurance—but that doesn’t mean you have to stay with the same company. Make it a habit to check your premium against your insurer’s competitors at least once a year.

You just might find you can get a better deal for the same level of coverage elsewhere. Small costs like this can add up without you realizing, so try to stay on top of it.

4. Be proactive about payments

Ultimately, it’s all about getting paid.

CPA consultancy Sobel & Co offered pointed to the following example in a recent whitepaper about cash flow management for retailers:

“Georgia Solotoff, owner of PIP Printing in Livingston bills her customers twice monthly. In addition to attaching the invoice to the finished product on delivery, she sends a copy of the invoice two weeks later. This not only has really accelerated collections but it keeps the company name in front of customers with more frequency.”

Part of this is offering multiple payment options (such as credit cards, electronic payments, buy-now-pay-later) to make it easier for customers to pay quickly.

5. Watch payment processing fees

Your customers have ever-changing preferences about how they like to pay.

And it’s in your best interest to help them do so in the easiest way possible—whether that’s by credit card, debit card, bank transfer or cash.

Yet, payment options like credit cards come with payment processing fees that can chip away at your sales revenue. Some fees can range from 1% to 4%. Drill down on these fees and look at switching payment processing providers, if you see a potential saving.

Further, when it comes to payment processing, consider whether your checkout process is streamlined. Reducing friction both online and in-store can improve the customer experience, helping to improve sales and reduce cart abandonment rates.

6. Audit common area maintenance (CAM) fees

You’re likely paying a common area maintenance (CAM) fee to maintain the common areas where you lease your commercial space if you’re operating as a brick and mortar retailer.

That can include things like the lighting, landscaping, driveways, janitorial services, exterior window cleaning and other management fees. It’s important that you know what you’re paying for in CAM fees, as this will need to be included in your operating expenses.

A CAM audit can help identify any excess fees, based on an analysis or your commercial lease and invoices. These fees can then be challenged and in some cases returned.

7. Keep cash reserves

A cash reserve is the money your business has set aside for any emergencies or unexpected costs. Think of it as your rainy day fund. Having a cash reserve can prevent your business from having to rely on credit cards to buy inventory or needing to seek finance to increase cash flow.

Cash flow management: the takeaways

So what does all of this mean for you as a retailer?

In short, getting on top of your cash flow position can be life-changing for both you and your business. Committing to improving your cash flow management can help retail businesses not only survive, but thrive.

Financial stability and reliability could improve your reputation among customers, suppliers and investors. A business that manages its cash flow effectively is seen as more trustworthy and capable, potentially leading to opportunities and partnerships that allow you to grow.

If you want to streamline your workflows and operate your retail business more efficiently, reach out to one of our Lightspeed Retail experts today.

Editor’s note: Nothing in this blog post should be construed as advice of any kind. Any legal, financial or tax-related content is provided for informational purposes only and is not a substitute for obtaining advice from a qualified legal or accounting professional. Where available, we’ve included primary sources. While we work hard to publish accurate content, we cannot be held responsible for any actions or omissions based on that content. Lightspeed does not undertake to complete further verifications or keep this blog post updated over time.

News you care about. Tips you can use.

Everything your business needs to grow, delivered straight to your inbox.